Planning on working during retirement? If so, you're not alone. An increasing number of employees nearing retirement plan to work at least some period of time during their retirement years.

Why work during retirement?

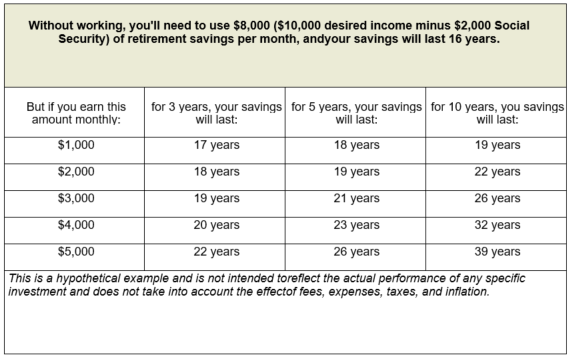

Obviously, if you work during retirement, you'll be earning money and relying less on your retirement savings — leaving more to potentially grow for the future and making your savings last longer, as shown in the example below:

Assumptions:

- Retirement savings: $1,000,000

- Earnings rate: 6%

- Preretirement income: $150,000

- Social Security: $2,000/month

- Desired income replacement: 80% ($120,000/year, $10,000/month)

If you continue to work, you may also have access to affordable health care, as more and more employers are offering this important benefit to part-time employees.

But there are also non-economic reasons for working during retirement. Many retirees work for personal fulfillment — to stay mentally and physically active, to enjoy the social benefits of working, and to try their hand at something new — the reasons are as varied as the number of retirees.

How working affects Social Security

If you work after you start receiving Social Security retirement benefits, your earnings may affect the amount of your benefit check. Your monthly benefit is based on your lifetime earnings. When you become entitled to retirement benefits at age 62, the Social Security Administration calculates your primary insurance amount (PIA), upon which your retirement benefit will be based. Your PIA is recalculated annually if you have any new earnings that might increase your benefit. So if you continue to work after you start receiving retirement benefits, these earnings may increase your PIA and thus your future Social Security retirement benefit.

But working may also cause a reduction in your current benefit. If you've reached full retirement age (66 to 67, depending on when you were born), you don't need to worry about this — you can earn as much as you want without affecting your Social Security retirement benefit.

If you haven't yet reached full retirement age, $1 in benefits will be withheld for every $2 you earn over the annual earnings limit ($19,560 in 2022). A special rule applies in your first year of Social Security retirement — you'll get your full benefit for any month you earn less than one-twelfth of the annual earnings limit, regardless of how much you earn during the entire year. A higher earnings limit applies in the year you reach full retirement age. If you earn more than this higher limit ($51,960 in 2022), $1 in benefits will be withheld for every $3 you earn over that amount, until the month you reach full retirement age — then you'll get your full benefit no matter how much you earn. (If your current benefit is reduced because of excess earnings, you may be entitled to an upward adjustment in your benefit once you reach full retirement age.)

Not all income reduces your Social Security benefit. In general, Social Security only takes into account wages you've earned as an employee, net earnings from self-employment and other types of work-related income, such as bonuses, commissions, and fees. Pensions, annuities, IRA distributions, and investment income won't reduce your benefit.

Also, keep in mind that working may enable you to put off receiving your Social Security benefit until a later date. In general, the later you begin receiving benefit payments, the greater your benefit will be. Whether delaying the start of Social Security benefits is the right decision for you, however, depends on your personal circumstances.

One last important point to consider: In general, your Social Security benefit won't be subject to federal income tax if that's the only income you receive during the year. But if you work during retirement (or receive any other taxable income or tax-exempt interest), a portion of your benefit may become taxable. IRS Publication 915 has a worksheet that can help you determine whether any part of your Social Security benefit is subject to federal income tax.

How working affects your pension

If you work for someone other than your original employer, your pension benefit won't be affected at all — you can work, receive a salary from your new employer, and also receive your pension benefit from your original employer. But if you continue to work past your normal retirement date for the same employer, or if you retire and then return to work for that employer, you need to understand how your pension will be affected.

Some plans will allow you to start receiving your pension benefit once you reach the plan's normal retirement age, even if you continue to work. Other plans will suspend your pension benefit if you work beyond your normal retirement date, but will actuarially increase your payment when benefits resume to account for the period of time benefits were suspended. Still other plans will suspend your benefit for any month you work more than 40 hours, and will not provide any actuarial increase — in effect, you'll forfeit your benefit for any month you work more than 40 hours.

Some plans provide yet another option — "phased retirement." These programs allow you to continue to work on a part-time basis while accessing all or part of your pension benefit. Federal law encourages these phased retirement programs by allowing pension plans to start paying benefits once you reach age 62, even if you're still working and haven't yet reached the plan's normal retirement age.

If your pension plan calculates benefits using final average pay, be sure to discuss with your plan administrator how your particular benefit might be affected by the decision to work part-time. In some cases, reducing your hours at the end of your career could reduce your final average pay, resulting in a smaller benefit than you might otherwise have received.

How working affects health benefits

Many individuals work during retirement to keep their medical coverage. If working during retirement means you will move from full-time to part-time, it's important that you fully understand how that decision will impact your medical benefits.

Some employers, especially those with phased retirement programs, offer medical coverage to part-time employees. But other employers don't, or require that you work a minimum number of hours to remain eligible for benefits. If your employer doesn't offer medical benefits to part-time employees, you'll need to look for coverage elsewhere. If you're married, the obvious option is coverage under your spouse's health plan, if your spouse works and has coverage available. If not, you may be eligible for COBRA.

COBRA is a federal law that allows you to continue receiving medical benefits under your employer's plan for some period of time, usually for 18 months, after a qualifying event (including loss of coverage due to a reduction in hours). But it's expensive — you typically have to pay the full premium yourself, plus a 2% administrative fee. (COBRA doesn't apply to employers that have fewer than 20 employees.) Other options are coverage through a state or federal exchange, or private health insurance.

Of course, once you turn 65, you'll be eligible for Medicare. You'll want to contact the Social Security Administration approximately three months before your 65th birthday to discuss your options.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

The information provided is not intended to be a substitute for specific individualized tax planning or legal advice. We suggest that you consult with a qualified tax or legal professional.

LPL Financial Representatives offer access to Trust Services through The Private Trust Company N.A., an affiliate of LPL Financial.

This article was prepared by Broadridge.

LPL Tracking #1-05114009